INSIGHT — The Discipline of a 12-Month Rolling Forecast

Financial Governance — Daleyn Accountancy

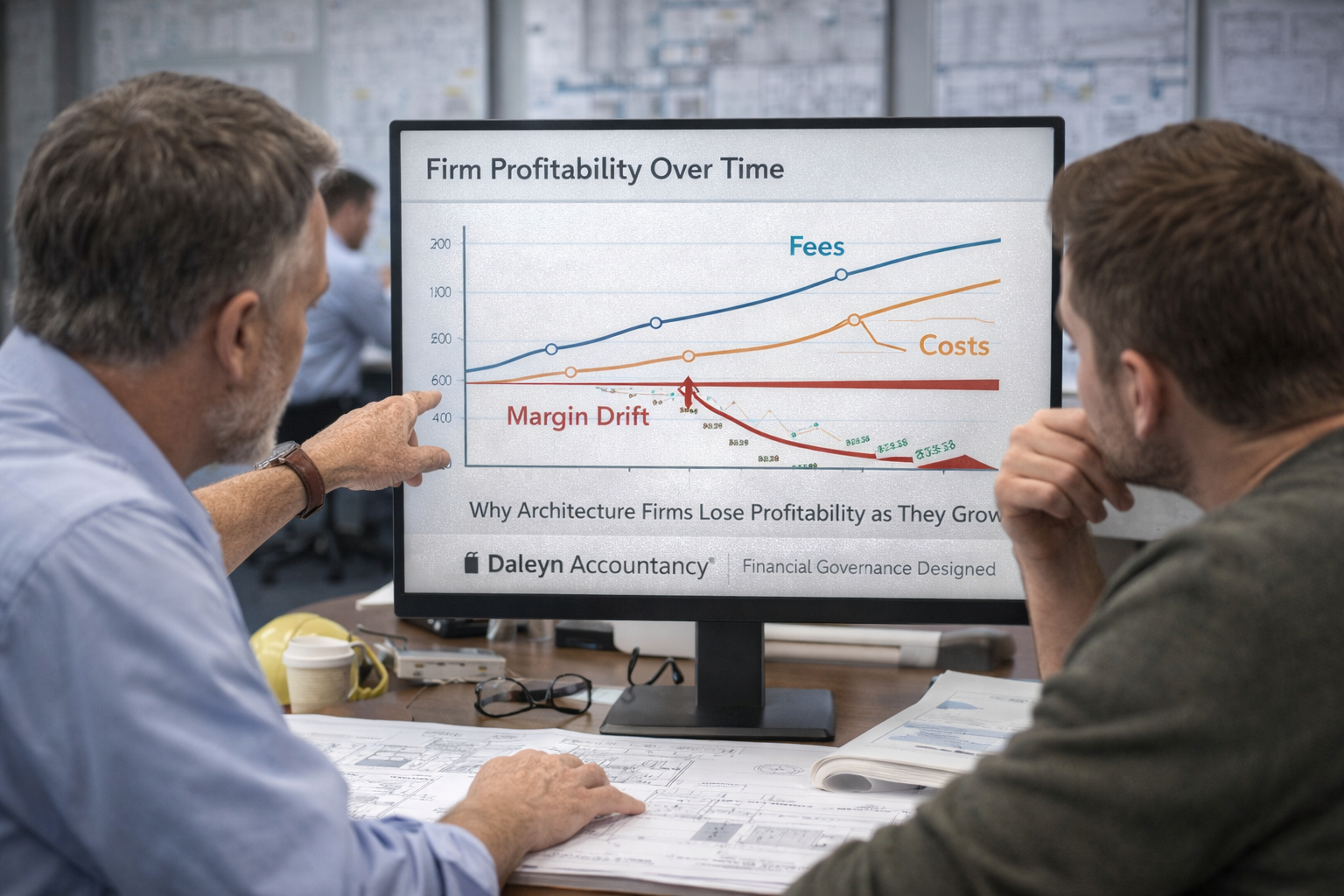

Architecture firms operate within an economic rhythm that rarely aligns with the calendar year. Project starts are shaped by procurement cycles, design phases evolve through iterative client decisions, and approvals from external authorities introduce delays that cannot be precisely controlled. Revenue does not follow a linear progression. It moves in response to the realities of project execution.

Despite this, many firms continue to rely on static annual budgets as the primary framework for financial planning.

At the beginning of the year, leadership establishes revenue expectations based on active projects and a reasonable view of the pipeline. Staffing levels are calibrated to those assumptions. Operating commitments are set accordingly. The budget, at that moment, reflects a coherent view of the firm's expected trajectory.

Yet architecture is not static.

By the second or third quarter, the conditions that informed the original plan have often shifted. Projects extend or accelerate. Client decisions introduce delays. Pipeline conversions occur at different intervals than anticipated. The financial model that once reflected reality begins to diverge from it.

The result is not simply forecasting error. It is a structural misalignment between how the firm plans and how it actually operates.

The Structural Problem

In many growing architecture firms, financial planning is treated as an annual exercise rather than an ongoing discipline. Once established, the budget remains largely unchanged, even as the operational environment evolves.

This creates a static planning structure within a dynamic business model.

The initial budget may be well constructed. It often reflects thoughtful assumptions about project timelines, staffing requirements, and anticipated commissions. However, architecture projects rarely proceed according to plan. Variability is not the exception—it is the operating condition.

Design timelines extend. Permitting processes take longer than expected. Clients adjust scope or delay approvals. In other cases, projects move more quickly, requiring earlier deployment of staff and resources.

As these changes accumulate, the gap between the original financial plan and the firm's actual trajectory widens.

Leadership may continue to reference the budget as a benchmark, even as it becomes less relevant to current conditions. Decisions around hiring, compensation, and investment are then made against a framework that no longer reflects the firm's forward position.

The issue is not that the budget was incorrect. It is that it was never designed to adapt.

Why It Occurs

This disconnect between planning and reality is not the result of poor oversight. It reflects structural characteristics inherent to architectural practice.

Project-Based Revenue Timing

Revenue is generated through milestone billing tied to project progression. Small shifts in design schedules or client approvals can move revenue across reporting periods. These shifts are often operationally minor but financially significant.

Fixed Operating Commitments

While revenue timing fluctuates, operating expenses remain comparatively stable. Salaries, office infrastructure, software platforms, and professional services continue regardless of billing cycles. As firms scale, this fixed cost base becomes more substantial and less flexible.

Evolving Project Pipelines

The pipeline is inherently fluid. New opportunities emerge, proposals advance or stall, and awarded projects may begin later than expected. These developments alter future revenue well before they are visible in historical reporting.

Decoupled Feedback Loops

Financial reporting captures outcomes after they occur. Planning, when static, does not incorporate real-time changes. This creates a lag between operational shifts and financial interpretation.

Together, these conditions create an environment where change is constant, but planning remains fixed.

Economic Implications for Architecture Firms

When financial planning does not evolve alongside operations, the firm's economic interpretation becomes increasingly distorted.

Leadership loses clarity on the firm's future position. Revenue expectations embedded in the annual budget no longer reflect current project schedules or pipeline realities.

Short-term fluctuations in billing may be misinterpreted. Periods of lower revenue—often the result of normal project timing—can trigger unnecessary cost reductions. Conversely, temporary surges may encourage premature hiring or expansion.

Without updated forecasts, staffing levels may drift out of alignment with actual workload. Overstaffing compresses margins. Understaffing constrains delivery and delays revenue realization.

Billing delays and shifting project timelines create uneven cash flow patterns. Without forward projection, these variations are difficult to anticipate and manage.

Over time, the absence of forward-looking discipline causes the firm to operate reactively. Decisions are made in response to recent performance rather than informed by expected conditions.

These outcomes are not the result of insufficient data. They stem from a planning structure that does not adapt to the underlying economics of the practice.

Introducing the Discipline of a Rolling Forecast

A 12-month rolling forecast introduces a governance framework designed to restore alignment between financial planning and operational reality.

Rather than relying on a static annual budget, the firm maintains a continuously updated projection extending twelve months forward. Each month, actual results replace prior assumptions, and the forecast extends outward to incorporate a new forward period.

This is not a revision of the budget. It is a structural shift in how the firm approaches planning.

The rolling forecast becomes a living model of the business—one that reflects current project schedules, staffing levels, and pipeline activity.

Within this framework, leadership examines the interaction of several core variables: the timing of project revenue as schedules evolve, staffing capacity relative to active and anticipated workload, pipeline progression and probability-weighted conversions, and the relationship between fixed operating commitments and expected income.

The objective is not precision. Architecture firms operate within too much variability for exact prediction. The objective is structured visibility.

By maintaining a current view of the next twelve months, leadership gains the ability to observe emerging patterns before they become financial constraints.

Governance Discipline in Practice

A rolling forecast is not simply a financial model. It is a governance discipline that requires consistency in how information is gathered, evaluated, and applied.

Project timelines must be regularly reassessed. Changes in design phases, client decisions, or approvals are reflected promptly in the forecast.

The forecast incorporates not only secured work but also the evolving pipeline. Opportunities are evaluated based on likelihood and timing, introducing a structured view of future revenue.

Staffing decisions are evaluated against projected workload. Hiring, redeployment, and capacity planning become informed by forward conditions rather than recent activity.

Forecasting relies on consistent assumptions regarding billing patterns, utilization rates, and project progression. This reduces variability in how projections are constructed across the firm.

Monthly updates reduce the lag between operational change and financial interpretation. Leadership can respond earlier, with greater precision.

Through these disciplines, forecasting becomes an integral component of financial governance rather than a periodic exercise.

Relationship to Financial Governance

The rolling forecast should not be viewed in isolation. It operates within a broader governance framework that aligns financial management with the economic structure of the firm.

As explored in Financial Governance vs. Financial Reporting, reporting alone cannot provide the forward visibility required to manage a project-based business effectively. Governance introduces structure, accountability, and real-time awareness.

The rolling forecast is one of the primary instruments through which that visibility is achieved.

It connects operational activity—projects, staffing, pipeline—to financial outcomes before they are realized. In doing so, it allows leadership to influence results rather than interpret them after the fact.

Without this forward-looking discipline, financial management remains anchored in historical reporting. With it, the firm gains a more active role in shaping its economic trajectory.

A More Stable Planning Framework

Architecture firms operate in an environment defined by long project durations, variable timelines, and collaborative delivery structures. Planning systems must accommodate this variability without sacrificing clarity.

A static annual budget provides an initial reference point, but it cannot absorb continuous change.

A rolling forecast introduces adaptability.

It does not eliminate uncertainty. Instead, it provides a structured method for incorporating uncertainty into financial planning. As conditions evolve, the forecast evolves with them.

Over time, this creates a more stable planning framework—one that reflects the actual rhythm of the practice rather than imposing a fixed structure upon it.

Measured Insight

The discipline of a 12-month rolling forecast is not about improving prediction accuracy. It is about maintaining alignment.

As architecture firms grow, the distance between planning and operations can widen if financial systems remain static. This distance introduces risk, reduces clarity, and encourages reactive decision-making.

A rolling forecast narrows that distance.

By continuously updating financial expectations, leadership gains a clearer understanding of where the firm is heading—not based on assumptions made at the beginning of the year, but on current conditions.

In mature practices, this level of visibility becomes essential. It allows financial planning to function not as a periodic exercise, but as an ongoing component of governance.

If your firm is evaluating its financial governance structure, we invite a private consultation.

Related Insights

More insights on architecture firm economics will be published here as part of this series.