Overhead Discipline in Growing Architecture Firms

Overhead Discipline in Growing Architecture Firms

Overhead Discipline in Growing Architecture Firms

Overhead is among the least examined financial dimensions of a growing architecture firm. It is accepted as a necessary cost of operation, allocated across projects as a percentage, and rarely subjected to the same level of scrutiny applied to staffing decisions or fee structures.

This acceptance is understandable in early-stage practices. When a firm is small and overhead is modest, its composition is transparent and its relationship to revenue is relatively stable. Leadership understands intuitively where the money is going.

As firms grow, this intuitive clarity disappears and the absence of a deliberate overhead governance framework becomes consequential.

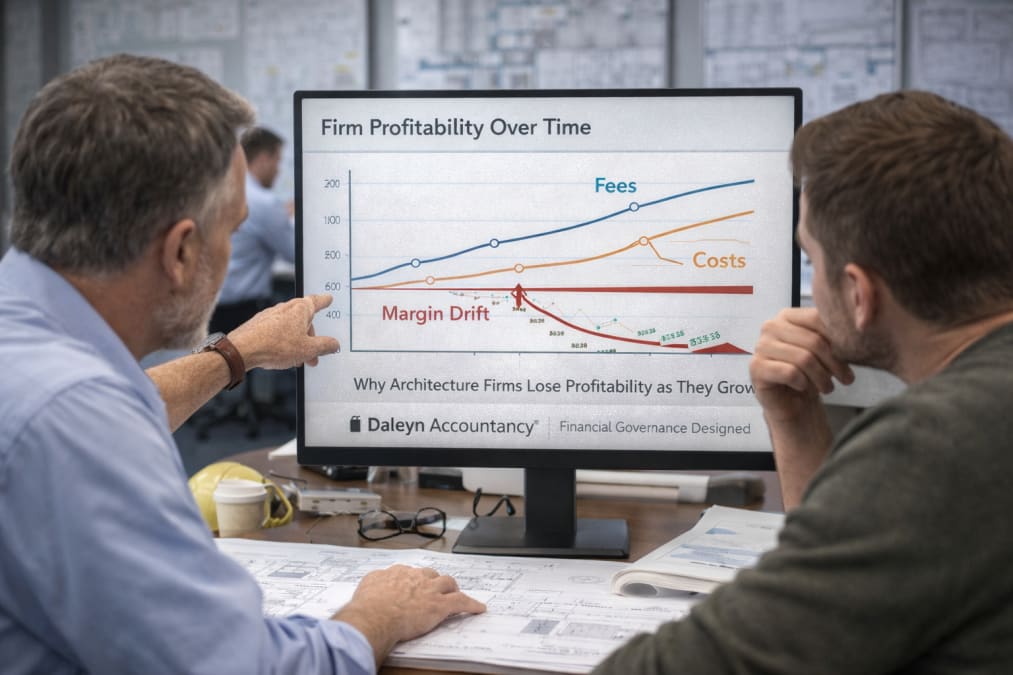

Overhead does not scale proportionally with revenue. It accumulates in layers, each one introduced for a legitimate operational reason, until the aggregate burden begins to exert a quiet but persistent pressure on profitability. By the time that pressure becomes visible in the income statement, it is already structurally embedded in the firm's cost base.

Understanding how overhead behaves during growth and developing the discipline to manage it intentionally is a core component of financial governance in architecture firms.

The Structural Problem: Overhead Grows in Increments That Each Seem Justified

Overhead does not arrive as a single, visible cost increase. It accumulates through a sequence of individually reasonable decisions each made in response to a genuine operational need.

A firm hires an office manager to handle administrative coordination that partners can no longer absorb. A project management platform is licensed to improve delivery consistency across a larger team. A marketing function is introduced to support business development at a scale that personal relationships alone can no longer sustain. A larger office is leased to accommodate growing headcount. A human resources process is formalized as staff numbers cross a threshold that makes informal management inadequate.

Each of these decisions is defensible. In the context in which it is made, it is probably correct.

The difficulty is that overhead decisions compound. Every fixed commitment added to the cost base must be supported by sufficient revenue and in a project-based business where revenue timing is irregular, the burden of that fixed base is felt acutely during slower periods.

More significantly, overhead commitments are rarely revisited once established. Costs that were introduced to support a particular scale of operations tend to persist even when the firm's revenue profile changes. They become structural fixtures rather than managed variables.

Over time, the overhead rate overhead as a proportion of net revenue drifts upward without a discrete moment at which leadership recognizes the shift. The firm has simply become more expensive to operate, and the margin available to partners after overhead and direct project costs has quietly contracted.

Why Overhead Accumulates Without Adequate Governance

The incremental accumulation of overhead is not a failure of judgment. It reflects structural characteristics of how professional service firms grow and how their financial management typically evolves.

Overhead decisions are made operationally, not financially

Most overhead additions in architecture firms are initiated by operational necessity. A project is delayed because of inadequate document management. Communication breaks down across a larger team. A key partner is spending too much time on administrative tasks.

The solution hire, license, lease is evaluated against the immediate operational problem. It is rarely evaluated against the firm's overhead rate, its revenue trajectory, or the cumulative effect of similar decisions made over the preceding twelve months.

Operational decisions and financial governance operate in separate conversations. Without a framework that connects them, overhead accumulates without deliberate design.

Fixed costs are introduced during periods of growth

Architecture firms typically add overhead during periods of strong revenue. A busy practice has the income to justify new commitments, and the operational pressure to act on them.

The difficulty is that the revenue supporting those commitments is often project-specific and not necessarily sustainable at the same level indefinitely. When project pipelines slow as they periodically do in a cyclical industry the overhead base established during the peak period remains in place.

Fixed costs do not retract when revenue contracts. They persist. And they consume a larger proportion of a smaller revenue base, compressing margins in exactly the periods when the firm is least equipped to absorb compression.

Overhead composition is not regularly examined

In many architecture firms, overhead is reviewed at the aggregate level total overhead as a line item on the income statement. The composition of that aggregate what it consists of, how each element has grown, and whether each commitment continues to serve its original purpose is examined infrequently, if at all.

Without compositional visibility, overhead management is reactive. Cuts are made under financial pressure rather than as are sult of proactive governance. The decisions made under pressure are often less precise than those made from a position of clarity.

The relationship between overhead and revenue is poorly understood

Overhead is often expressed as a fixed dollar amount. It is more usefully understood as a rate overhead as a proportion of net revenue because this framing reveals how operational costs are scaling relative to the firm's income-generating capacity.

When overhead grows at the same rate as revenue, the burden is stable. When overhead grows faster than revenue which it frequently does during periods of organizational expansion the margin available for profitability and partner distributions contracts, even if total revenue is increasing.

This relationship is not always visible to leadership unless it is explicitly tracked.

Economic Implications for Architecture Firms

The consequences of unmanaged overhead accumulation extend across the firm's financial structure.

Profitability becomes structurally constrained. When overhead consumes an increasing proportion of revenue, the margin remaining after direct project costs and overhead narrows. The firm may be generating strong top-line growth while delivering diminishing returns to its partners. Revenue and profitability decouple a condition that can persist for years before leadership recognizes its source.

The firm's resilience to revenue variability declines. A firm with a lean overhead structure can absorb a slow quarter with relative stability. A firm with a heavy fixed cost base has less tolerance for the same variability. In a project-based industry where revenue timing is inherently irregular, overhead discipline is directly correlated with financial resilience.

Hiring decisions become more consequential than they appear. Every addition to the permanent staff base adds to fixed overhead not only in salary but in the associated costs of employment, management, and infrastructure. In isolation, each hire is a manageable commitment. In aggregate, permanent headcount is typically the largest component of overhead and the one most difficult to reduce without significant disruption.

Growth requires more revenue to maintain the same level of profitability. As overhead increases, the revenue threshold required to achieve a given level of profit rises. A firm that needed two million dollars in revenue to deliver strong profitability at one scale may need three million to deliver the same result at a larger scale not because it is less efficient, but because its cost base has expanded. Understanding this relationship is essential for setting realistic growth expectations.

Introducing Financial Governance Discipline

Overhead discipline is not about minimizing costs. It is about ensuring that overhead commitments are made intentionally, monitored consistently, and evaluated against the revenue capacity of the firm.

Track the overhead rate as a primary governance metric. Overhead expressed as a proportion of net revenue rather than as an absolute dollar figure provides a more meaningful basis for governance. This rate should be monitored at regular intervals and understood in the context of the firm's revenue trajectory. A rising overhead rate during a period of strong revenue growth warrants examination. The same rate during a period of revenue contraction warrants immediate attention.

Establish compositional visibility. The aggregate overhead figure should be broken down into its constituent elements occupancy, administrative staff, technology, marketing, professional services, and principal non-billable time and each element should be understood as an individual commitment with its own cost trajectory. This compositional view allows leadership to identify where overhead is growing most rapidly and whether that growth is proportionate to the operational value being delivered.

Evaluate overhead commitments against revenue scenarios, not just current performance. Before adding a fixed cost a new hire, a lease extension, a technology platform - the decision should be evaluated against a range of revenue scenarios, not only the current one. What does this commitment cost if revenue contracts by fifteen percent? By twenty-five percent? This forward-looking stress test does not prevent necessary investment. It ensures that commitments are made with awareness of their implications under conditions that are not merely optimistic.

Distinguish between growth-enabling overhead and operational drift. Not all overhead accumulation is problematic. Some overhead investments in systems, in talent, in infrastructure - create the capacity for revenue growth that would not otherwise be achievable. The governance discipline is in distinguishing these investments from overhead that has accumulated through operational momentum rather than deliberate design. The former deserves to be evaluated on its return. The latter deserves to be examined for reduction or elimination.

Conduct an overhead review on a defined annual cycle. Rather than waiting for financial pressure to prompt scrutiny, firms that govern overhead well schedule a structured annual review of their cost base. This review examines each overhead element, its growth trajectory over the prior year, and its continued alignment with the firm's operational requirements. Commitments that no longer serve their original purpose are identified and addressed before they become entrenched.

The Connection to Governance and Utilization

Overhead discipline does not operate independently of the other financial governance dimensions examined in this series.

As explored in the financial governance vs. financial reporting article, aggregate reporting alone does not reveal the structural dynamics shaping a firm's economic performance. Overhead is precisely the kind of structural variable that can drift significantly within aggregate figures without triggering immediate concern until its cumulative effect becomes unmistakable.

Overhead also interacts directly with utilization. When overhead is heavy, the utilization threshold required to sustain profitability rises. A firm that might achieve acceptable margins at sixty-five percent billable utilization under a lean overhead structure may require seventy-five percent or more under a heavier one. Understanding this relationship allows leadership to set utilization targets that reflect the firm's actual cost structure rather than industry benchmarks that may not apply

Together, overhead discipline and utilization management form two of the foundational governance pillars of a financially resilient architecture practice.

A Measured Perspective

Growing architecture firms accumulate overhead because they are growing. This is not a flaw it is the natural consequence of building organizational capacity.

The discipline required is not restraint in the face of growth. It is intentionality in the management of what growth creates.

Firms that develop overhead governance that track their overhead rate with regularity, examine the composition of their cost base, and evaluate new commitments against a range of revenue scenarios are better positioned to grow sustainably. They understand what their growth costs, what it requires in terms of revenue, and what margin remains after those costs are met.

This understanding does not constrain strategic ambition. It grounds it in financial reality which is precisely where ambition is most likely to produce durable results.